Use our AI search to ask us a question or use keywords to search for pages or documents.

Example: "How do I apply for a financial institution licence?", "FMA Annual Report 2024"

Like many organisations, we use technology on our website to collect information that helps us enhance the experience of our site. The cookies we use allow our website to work and help us to better understand what information is most useful to you.

The story goes that Albert Einstein once called compound interest the eighth wonder of the world, saying “He who understands it, earns it; he who doesn't, pays it”. Whether or not those are actually his words, it’s true that compound interest is a powerful effect of investing that, over time, will get your money working for you.

When you invest money in a product such as a term deposit or managed fund, you are (in simple terms) lending your money to someone who will use it to (hopefully!) make more money. Interest is money paid to you by a borrower in return for you lending your money.

Depending on the terms of your investment, when interest is paid out, it may be added to the overall sum you have invested. This gives the interest the opportunity to compound, which basically means you earn interest on that interest.

For example You invest $10,000 in a product that offers a fixed return of 4% per year (for the purposes of this example, calculated annually, and after fees and tax). At the end of the year, you will receive $400 in interest – 4% of $10,000.

You keep in the entire $10,400 in the investment. At the end of the second year, you receive $416. That is 4% on your original investment, and also 4% on the interest you earned last year – for a total of $10,816. That $16 is compound interest.

Compound interest is for the long term An extra $16 doesn’t sound like much. But the real value of compound interest is over the long term.

If you kept the above example invested for 10 years, by the end you would have $14,802 – your original $10,000, $4000 from interest, and $802 from interest on the interest.

Now imagine you made additional contributions to the investment each month or year, or kept the money invested for even longer (the amount of time you might save for retirement, for example). You can start to get an idea of how the increases grow.

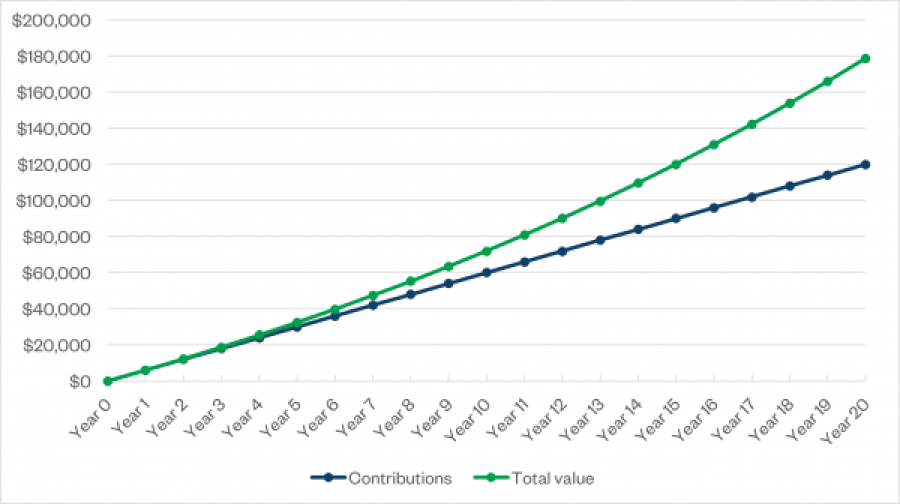

Here’s an example for visual learners:

The graph shows someone investing $500 per month for 20 years, and earning a fixed rate of 4% interest per year. Notice the total value line slopes up ever more sharply than the contributions? Think of that steeper angle as compound interest at work, providing returns on the returns, while the amount contributed stays the same.

Time is obviously the key factor. The longer you’re invested, the further apart the lines get. So, the sooner you get started, the greater the benefits will be.

The compounding effect is the same for investment products like managed funds, with returns rather than interest. However, as returns are based on the value of the fund’s underlying investments, the total value of the investment may fluctuate as markets rise and fall.

KiwiSaver uses the benefit of compounding returns. Because you cannot access your money until you turn 65, returns automatically become part of your investment, and instantly start generating returns themselves.

The Savings Calculator on sorted.org.nzlets you plug in your own numbers to see how compound interest could play a part in your savings goals.

Compounding is a side effect

Remember, compounding interest or returns aren’t a product or separate feature. They’re theeffectof reinvesting your investment returns. It becomes part of your overall investment, and therefore subject to the same returns and risks. If the market dips and the value of your KiwiSaver investment drops, that drop applies to your total investment – your contributions and the returns earned.