Educative and constructive approach

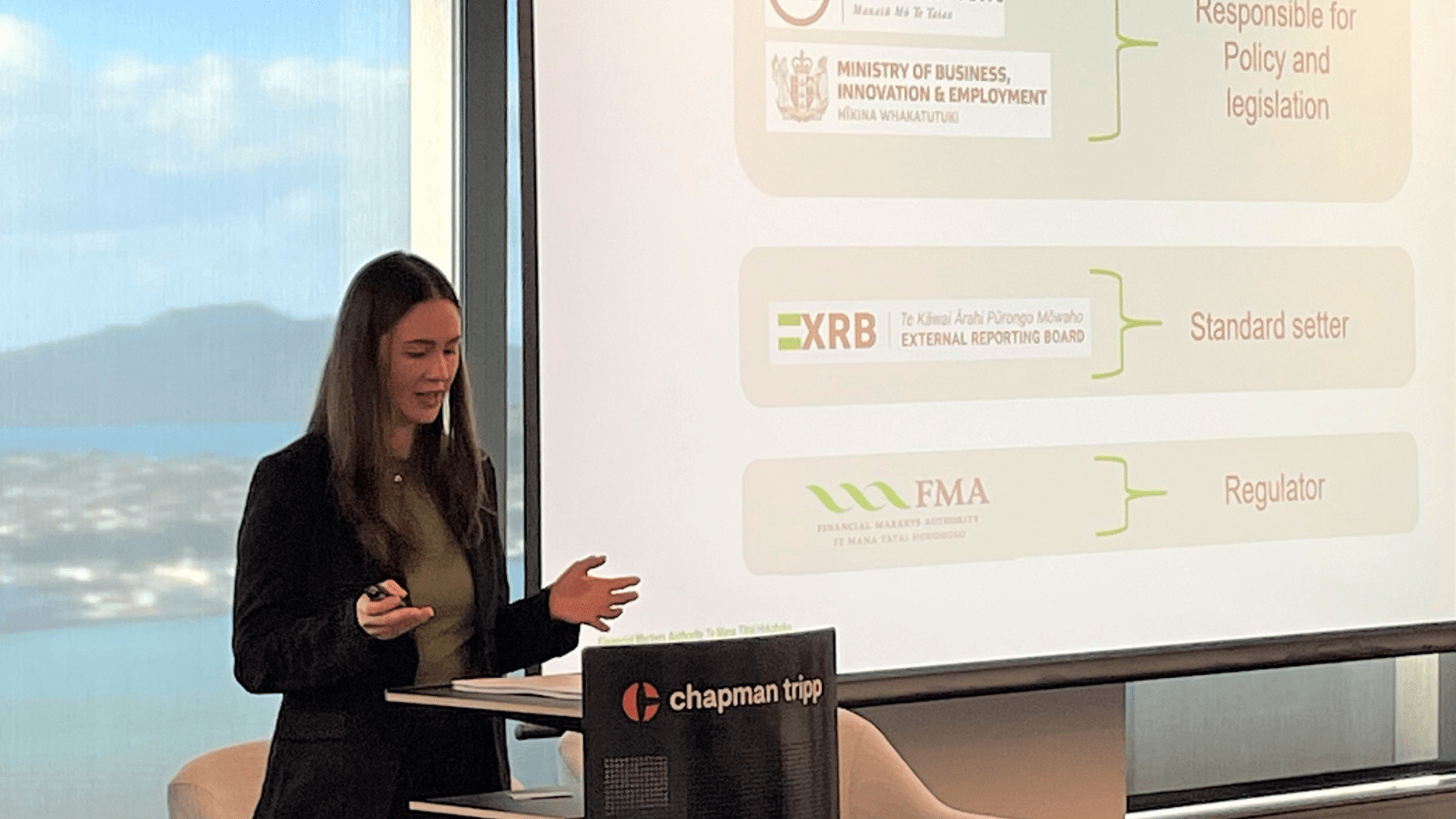

As the regulator, the FMA will monitor and enforce the new regime, provide guidance, and share feedback to improve the level of reporting over time. “Our role is to ensure that what Climate Reporting Entities (CREs) disclose can be substantiated,” explained Jenika. “It’s how the FMA can ensure the regime contributes to Aotearoa New Zealand’s transition to a more sustainable, low emissions economy.”

Four new pieces of guidance covering monitoring, third-party providers, record-keeping, and scenario analysis are due out in June and July 2023.

As the first climate statements are published in 2024, the FMA will support CREs to improve but will also take enforcement action where they fail to produce a climate statement or where information is false or misleading. There are criminal and civil (financial) penalties for those who don’t comply.

Jenika noted that adapting to the new record-keeping requirements will be a challenge for many entities. CREs must be able to prove what they report is true. To do this, they will need to determine what new climate-related data and information is required to substantiate the climate statements produced for their entity, and identify ways to collect, analyse and store it.

Jenika advised the audience to start preparing now: “This is a significant change. It may require more resources, new processes, and systems, and some upskilling across your organisation. Our advice is don’t delay. Start preparing now.”

Climate risk and financial statements

There are obligations for entity’s, regardless of whether they fall under the CRD regime, to determine whether climate has an impact on their financial statements and other communication, such as product disclosure statements.

Directors and management teams are responsible for ensuring financial statements comply with the Accounting Standards and that means including climate in their risk assessment processes if they are material.

Transparency is key as Jacco explained: “Entities may want to disclose how they have considered climate risk even if it didn’t have a material impact on their numbers. Users expect to see it and may wrongly assume it’s not been considered if it’s not disclosed.”

The FMA issued guidance for auditors on what it expects to see in audit files on material climate risks in October, which may also be useful for entities. From the 2023 reporting season, the FMA’s monitoring of financial reporting and audit quality reviews will include consideration of climate risks, and how these have been addressed, and its monitoring approach will ensure that climate-related disclosures are consistent across multiple documents including financial statements.

Learn more about the climate-related disclosures regime

Sign up for climate-related disclosure news and updates by selecting Climate Reporting Entity (CRE) information from the subscription checklist